Financial sector partners

Visa Air Europa Suma¹ bankintercard

Exchange and earn miles simply with your Air Europa Suma card.

bankintercard, the credit card brand of Bankinter Consumer Finance, together

with Air Europa, has created a payment card with many advantages in the travel

sector: the Visa Air Europa Suma Card.

Visa Air Europa Suma Card customers can earn Miles for every purchase they

make with the card and add them to those accumulated in the Air Europa Suma

Programme

What are you waiting for to start collecting Miles?

You will be redirected to a Bankinter Consumer Finance website.

Product distributed by Air Europa Líneas Aéreas S.A.U

¹Credit cards issued by Bankinter Consumer Finance, E.F.C., S.A., a Hybrid

Payment Institution registered with the Bank of Spain under number 8832, with its

registered office at Avda. de Bruselas 12, 28108 Alcobendas (Madrid), and

registered with the Madrid Commercial Registry under T. 22.729, F. 181, H. M-

259543 and CIF A82650672. The safeguarding system chosen by Bankinter

Consumer Finance to protect the funds received from its customers, or through

another payment service provider for the execution of payment operations, is

subject to the legally established procedure, consisting of depositing them in a

sight account separate from that of Bankinter, S.A. Standardised European

Information (I.N.E.) and quarterly information on applied commissions and rates

available at bankintercard.com

Two Payment options:

• Deferred Payment ("Revolving") You can pay in instalments (20.55%

N.I.R., 22.60% A.P.R.2)

• End of Month Payment

| AIR EUROPA PURCHASES | OTHER PURCHASES |

|---|---|

| 3 Miles for every euro spent |

0,5 Miles for every euro spent |

The Suma Miles associated with monthly spending will be credited during the first week of the month following the purchase.

Welcome Promotion:

Up to 12,000 welcome bonus Miles to go further

6,000 Miles the first year When you spend €100 in each of the first 6 monthly settlement periods.

6,000 Miles the second year When you spend €100 in each of the first 6 monthly settlement periods.

Maximum bonus: 1,390 Miles/monthly settlement period

Advantages of your Visa Air Europa Suma Card:

• Regardless of your bank. Simply link the card to your usual account.

• Flexible payment. You can pay in Deferred Payment ("Revolving") or End of Month Payment.

• Transfer money to your current account. You will have cash in just 48 hours. This transaction does not generate Suma Miles.

• Free alert service. Every time you make a transaction with your card, you will receive a confirmation message. Additionally, you will receive SMS notifications about the next charge date on your account.

• Discounts on your purchases at over 12,000 establishments

Card issued by Bankinter Consumer Finance EFC, S.A. See conditions

*In case of cancellation of the Visa card, the Suma Silver level benefit obtained with the card’s issuance and/or promotion will be automatically revoked.

IMPORTANT INFORMATION This card is a "Revolving" credit card that allows you to use your credit limit to finance purchases, cash withdrawals or cash transfers to your current account, repaying the credit in monthly instalments that include principal and interest. The contract is for an indefinite duration, although you can terminate it at any time by repaying the outstanding balance in a lump sum to cancel the card. The entity can also resolve it with a minimum of 2 months' notice. Please note that if you decide to sign up for the card, if you choose a very low monthly payment, it could take you longer to pay off the outstanding balance and you could end up paying more in interest. In addition, the available credit limit is automatically renewed each month, hence the term "Revolving".

The available credit limit decreases with the charges from the withdrawals you make with the card and is replenished with payments you make through the monthly instalments. Therefore, we remind you that if you increase the number of withdrawals and continue paying the same monthly instalment amount, the amortization of the loan would be prolonged and would result in the payment of a high amount of interest.

CREDIT LIMIT: up to €5,000.00. The credit limit will be the one assigned by the Entity according to the credit and payment capacity analysis carried out on the Holder.

PAYMENT METHODS: When activating the Card, the Holder must choose one of the Card's general payment methods. If you select the Deferred Payment ("Revolving") option, you will also have to choose the percentage or fixed amount you wish to pay each month, always respecting the minimum amount established for this payment method.

(i) General payment methods:

a) End of Month Payment: Transactions made with the Card, including those exceeding the credit limit, are paid in full at the end of the monthly Settlement Period. No interest is applied; however, fees and expenses generated in that Settlement Period are passed on (3.19% APR).

b) Deferred Payment ("Revolving"): It allows the Cardholder to pay in instalments for transactions made with the Card. The Holder can choose between paying monthly: (i) a fixed amount, with a minimum of 40.00 euros; or (ii) a percentage of the Outstanding Balance, from 3.00% to 99.99%. Unlike the End of Month Payment option, not all the credit used is paid off at the end of the monthly Settlement Period.

Instead, that amount is paid across several instalments, depending on the option selected by the Holder; interest will accrue from the moment at which the transaction is performed.

Minimum requirements. The final amount to be paid:

- May not be less than 40.00 euros or 3.00% of the Resulting Balance.

- Shall be equal to at least 0.35% of the Principal Drawn, excluding amounts over the credit limit.

- It will include all interest generated during the Settlement Period.

Therefore, that amount could be higher than that of the chosen option.

To this amount will be added the rest of the items that make up the monthly fee, that is:

- the full balance of any overdrafts incurred;

- The commissions and expenses generated;

- And the instalments of the transactions that were carried out under the special payment methods.

It is advised that in the Deferred Payment ("Revolving") option, the smaller the fixed amount or percentage chosen, the more time you will need to pay off your debt. This is because, with small amounts, a smaller portion of the monthly payment is allocated to repaying the principal.

As a result, you'll end up paying more and for a longer period of time.

(ii) Special payment methods. The Holder can also defer specific transactions using one of the following special payment methods. In these cases, the conditions of the special payment method apply exclusively to the transaction selected, while the remaining transactions continue to be repaid as per the established general payment method:

a) Payments in instalments ("Split Purchases"): It allows the Holder to postpone payment for a specific transaction (or several grouped together). The Holder can choose:

(i) the instalment amount you wish to pay each month;

Or (ii) the number of months over which you want to defer payment of the transaction.

Deferral conditions:

- The minimum amount that must be deferred will be 90.00 euros (or the minimum that is established at any given time).

- Payment can be split into 3 to 36 months (or the options that are available at any given time). This period may be extended by an initial grace period on the principal that will run from the date on which the postponement is requested until the end of the Settlement Period in which the postponement was made.

- Commission charges cannot be financed under this payment method.

- The monthly instalments will be the same amount, except: The first instalment, because it may only include the interest generated during the initial grace period;

- And the final instalment, with a view to adjusting the amount to be repaid across the number of instalments selected as part of the transaction.

Minimum conditions. The chosen or resulting monthly instalment shall not be less than 30.05 euros (or the minimum amount determined at any given time).

b) Deferred Payment in Stores: allows the Holder to defer payment of purchases made at stores offering this option.

Deferral conditions:

- The minimum amount that must be deferred will be 60.00 euros (or the minimum that is established at any given time).

- The payment can be split into 3, 6, 9 or 12 months (or the options that are available at any given time).

- The monthly instalments will be of equal amount, except for the last instalment, to adjust the amount to be repaid among the number of instalments chosen in the transaction.

This payment method will only be available if, at the time of the transaction, the general End of Month Payment option has been selected for Card repayments.

(iii) Changes to payment methods. The Cardholder can change the general payment method they have chosen from among the different options available on the Card. If you have the Deferred Payment ("Revolving") option, you can also modify the percentage or fixed amount you must pay monthly with the Card, always respecting the minimum conditions allowed for that option. These changes can be made up to five (5) calendar days before the end of the current Settlement Period, through the following channels: phone: 900 811 311; web: www.bankinterconsumerfinance.com; App; or any other channel enabled by the Bank.

Nominal interest rate (NIR)

(i) General end-of-month payment method: interest free (3.19% APR).

The indicated APR has been calculated under a provision for purchases in stores. Representative example under the assumption that the Contract remains in force throughout its term and the Parties fulfil their obligations under the agreed conditions and deadlines. If, from the first day of the Contract's term, you make purchases worth €1,500.00 over a period of 12 months, to be repaid over 12 months at the end of each of the Settlement Periods (monthly), with a maintenance fee of €48.00 for the Card and a fixed annual nominal interest rate of 0.00% (3.19% APR): the total amount payable would be €18,048.00 (€18,000.00 of principal and €48.00 of fees), through 12 monthly instalments of €1,500.00 each (€1,500.00 of principal). This fee will be accrued annually, after one year has elapsed since the Card was issued. It will be settled in the bill corresponding to the Settlement Period in which that Card was issued. Total cost of credit: €48.00.

(ii) Under the general Deferred Payment (“Revolving”) method for purchases and cash transfers to your current account: 20.55% NIR. (22.60% APR).

Representative example under the assumption that the Contract will remain in force throughout its term and the Parties will fulfil their obligations under the agreed conditions and deadlines. For a purchase or cash transfer of €1,500.00 to your current account, made on the first day of the settlement period under the Deferred Payment ("Revolving") method, with a 4-year repayment period, to be repaid through 48 equal monthly instalments calculated based on the constant instalment repayment system. With the application of the fixed annual nominal interest rate: 20.55% (22.60% APR). In this case, the total amount payable would come to €2,212.04 (€1,500.00 of principal and €712.04 of interest), in 47 monthly instalments of €46.09 (the first instalment for €20.40 of principal and €25.69 of interest) and a final instalment of €45.81 (€45.04 of principal and €0.77 of interest). Total cost of credit €712.04.

(iii) General Deferred Payment ("Revolving") method for an ATM cash withdrawal against credit: 13.58% NIR. (16.98% APR).

Representative example under the assumption that the Contract remains in force throughout its term and the Parties fulfil their obligations under the agreed conditions and deadlines. For a withdrawal of €1,500.00 on the first day of the settlement period, to be repaid over 48 months in fixed instalments, with an ATM cash withdrawal fee of 4.00% of the amount drawn down (min. €3.00) and with the annual nominal interest rate of 13.58% (16.98% APR): the total amount to be paid would be €2,012.42 (€1,500.00 principal, €452.42 interest, and €60 fee), through a first monthly payment of €100.67 consisting of the first monthly instalment of €40.67 (€23.69 principal and €16.98 interest) and €60 fee; 46 monthly instalments of €40.67 (the first of these 46 instalments consisting of €23.96 principal and €16.71 interest); and a final instalment of €40.93 (€40.47 principal and €0.46 interest). Total cost of credit: €512.42.

(iv) In the special modality of Payment in Instalments (Split Purchases): 20.55% NIR. (22.60% APR). The indicated APR may vary depending on the day of the contract settlement period.

Representative examples under the assumption that the Contract remains in force throughout its term and the Parties fulfil their obligations under the agreed conditions and deadlines. For a drawdown of €1,500.00, deferred on the first day of the billing period, to be repaid within 12 months under the constant instalment system and at a fixed annual nominal interest rate of 20.55% (22.60% APR). Based on this assumption, the total amount payable would be €1,684.18 (€1,500.00 of principal and €184.18 of interest), through a first instalment of €25.69, with a first instalment solely of interest, and 10 monthly instalments of €150.77 (the first of these 10 instalments being composed of €125.08 principal and €25.69 interest) and a final instalment of €150.79 (€148.25 principal and €2.54). Total cost of credit €184.18.

(v) Special deferred payment in stores: 20.55% NIR. (22.60% APR). The APR indicated may vary depending on the day of the contract settlement period.

Representative example under the assumption that the Contract remains in force throughout its term and the Parties fulfil their obligations under the agreed conditions and deadlines. For a withdrawal of €1,500.00, made on the first day of the settlement period, to be repaid within 12 months under the system of constant instalments, at a fixed annual nominal interest rate of 20.55% (22.60% APR). In this case, the total amount payable would be €1,672.17 (€1,500.00 principal and €172.17 interest), through 11 monthly instalments of €139.35 (the first 11 of these instalments composed of €113.66 principal and €25.69 interest) and a final instalment of €139.32 (€136.97 principal and €2.35 interest). Total cost of credit €172.17.

SIMULATOR. Simulate the payment of the last instalment. Consult the Bank of Spain simulator, or our simulator, to calculate the end date of the final instalment.

CONSEQUENCES IN CASE OF NON-PAYMENT. If you do not pay the amount owed within the agreed deadlines, late payment interest will accrue and you will have to pay the expenses incurred by your bank in seeking recovery of the amounts owed. If this non-payment persists over time, Bankinter Consumer Finance may claim the debt through legal channels, which will entail additional expenses for you. Furthermore, in the event of non-payment, Bankinter Consumer Finance may communicate your data to the credit information systems to which it is affiliated, which may make it more difficult for you to access financing or new loans in the future.

RIGHT OF WITHDRAWAL. You can decide to cancel your card within 14 days of its activation, without the need to give any reason and at no additional cost. In that case, you could let us know by calling the phone number shown on the card. If you have made any drawdown during those 14 days, you must return the capital drawn down and the accrued interest within a maximum period of 30 calendar days from the date on which the withdrawal notice is sent and return the card accordingly.

QUARTERLY INFORMATION. You can consult the quarterly information on the fees and rates most commonly offered by Bankinter Consumer Finance E.F.C., S.A.U. at: https://www.bankinterconsumerfinance.com/nosotros/información-clientes. For further information about the calculation of interest, the structure of the different payment methods and the services associated with the Card, consult the General Terms and Conditions of the Contract or the European Standardised Information Sheet (ESIS) and other pre-contractual information (Spanish, Catalan, Basque, Galician and Valencian).

ADDITIONAL BENEFITS. Accumulation of miles as part of the Air Europa Suma loyalty programme with every purchase you make: 3 Miles for every euro spent on direct purchases of Air Europa tickets and 0.5 Miles for every euro destined to other purchases. This benefit applies regardless of the payment method used. The maximum bonus in miles is 1,390 miles/monthly settlement period. These Miles will be accumulated in favour of the main holder of the Air Europa Suma Visa Credit Card within the Air Europa Suma Plan. These conditions only apply to purchases made with the card at stores. They will not apply to other operations such as: cash withdrawals at ATMs; top-ups or prepaid card purchases; money transfers; credit of fees or taxes; buying and selling of crypto assets; loan transactions; money transfers to your current account; transactions undertaken or financed using platforms or payment instruments other than the Entity that are associated with the Card; or any other transaction that is not intended for the acquisition of goods or services.

WELCOME OFFER. Bonus of up to 12,000 Miles, distributed over two periods:

First period: 6,000 Miles. Make a minimum spend on purchases of €100.00 using the Card in each of the first 6 settlement periods, starting from the date on which the card was issued (figure that appears in the communication that the Bank sends along with the card), regardless of the payment method used. If that minimum expenditure is not reached in any of the monthly settlement periods, the bonus corresponding to that period will not be obtained. Miles will be credited to the Air Europa Suma account of the main holder the month following the fulfilment of the conditions.

Second period: 6,000 Additional Miles. Starting from the 13th settlement period after the card is issued, you must spend a minimum of 100€ on purchases in each of the following 6 settlement periods. If the minimum spend is not reached in any period, the Miles corresponding to that period will not be earned. The Miles will be credited into the Air Europa Suma account of the primary holder the month following the month in which the conditions are fulfilled.

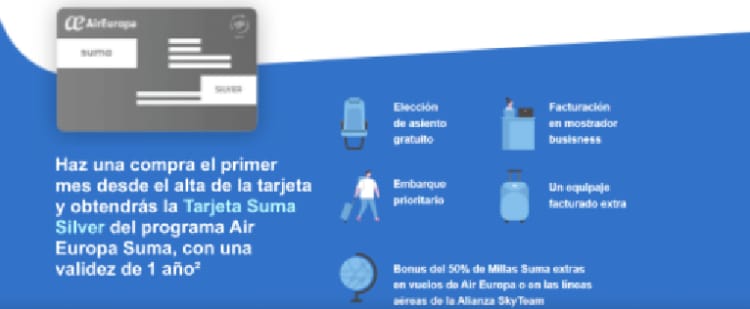

2 If you make a purchase in the first month following the card registration date (as shown in the correspondence sent by the Bank with the Card), you will be entitled to one year of the Suma Silver Card as part of the Air Europa Suma programme. The Suma Silver Card will be renewed annually if 3,000 Suma Miles are earned within a one-year period through spending with the Air Europa Suma Visa Card.

Any operations related to the Air Europa Suma Visa Card must be carried out

through the bankintercard customer service helpline at 900 811 311